Dynamic labor supply

A simple numerical model

We are going to cover the first steps to solving and simulating a dynamic programing problem. We consider a labor supply problem with asset and simple choices over hours. We will allow for sthochastic productivity. We are going to consider here a finite horizon problem.

The decision problem for the agent is to choose every period, how much to consume, how much to work and how much to save. We are going to solve this at a yearly frequency over 50 years.

Setting the environment

The state space is given by age, producitivity and asset level. We consider the separable utility function over leisure and consumption. We fix all parameters. WE also consider a simple end of life value.

We prepare the wage realizations in each state and the value function.

p = list(nx=30,na=40,nb=100,nh=10,gamma = 2, eta=-1.5 , lambda=0.1,r=0.02,beta=5,fc=1)

V = array(0,c(p$na,p$nx,p$nb))

X = exp( qnorm((1:(p$nx))/(p$nx+1)))

B = c(0,exp(seq(log(min(X)),log(max(X/p$r)),l=p$nb-1)))

H = seq(0,1,l=p$nh)

wage = X

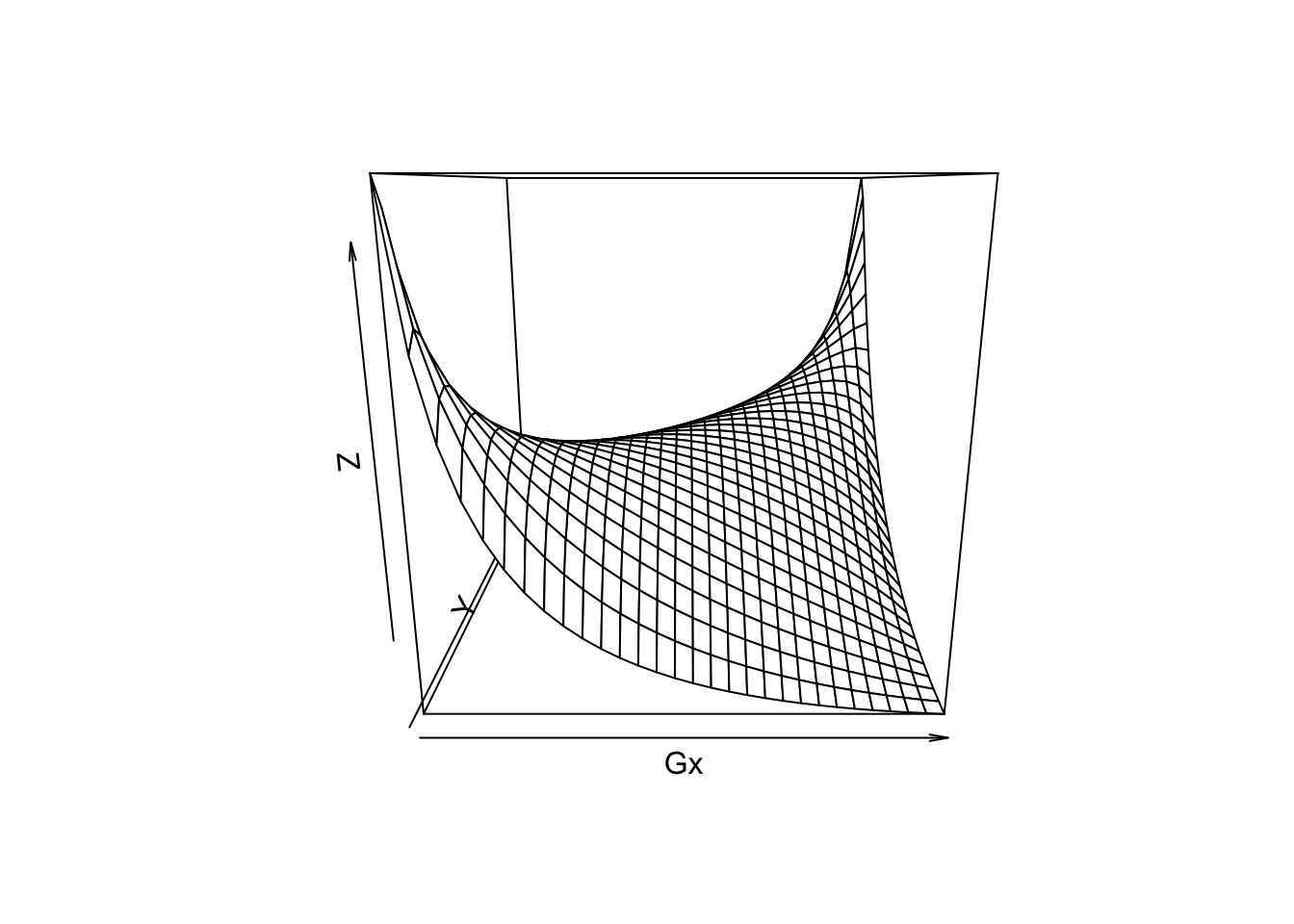

# transition matrix on productivity

X1 = spread(X,1,p$nx);X2 = spread(X,2,p$nx);

Gx = dnorm(log(X2)-log(X1))

Gx = Gx/spread(rowSums(Gx),2,p$nx)

persp(Gx)

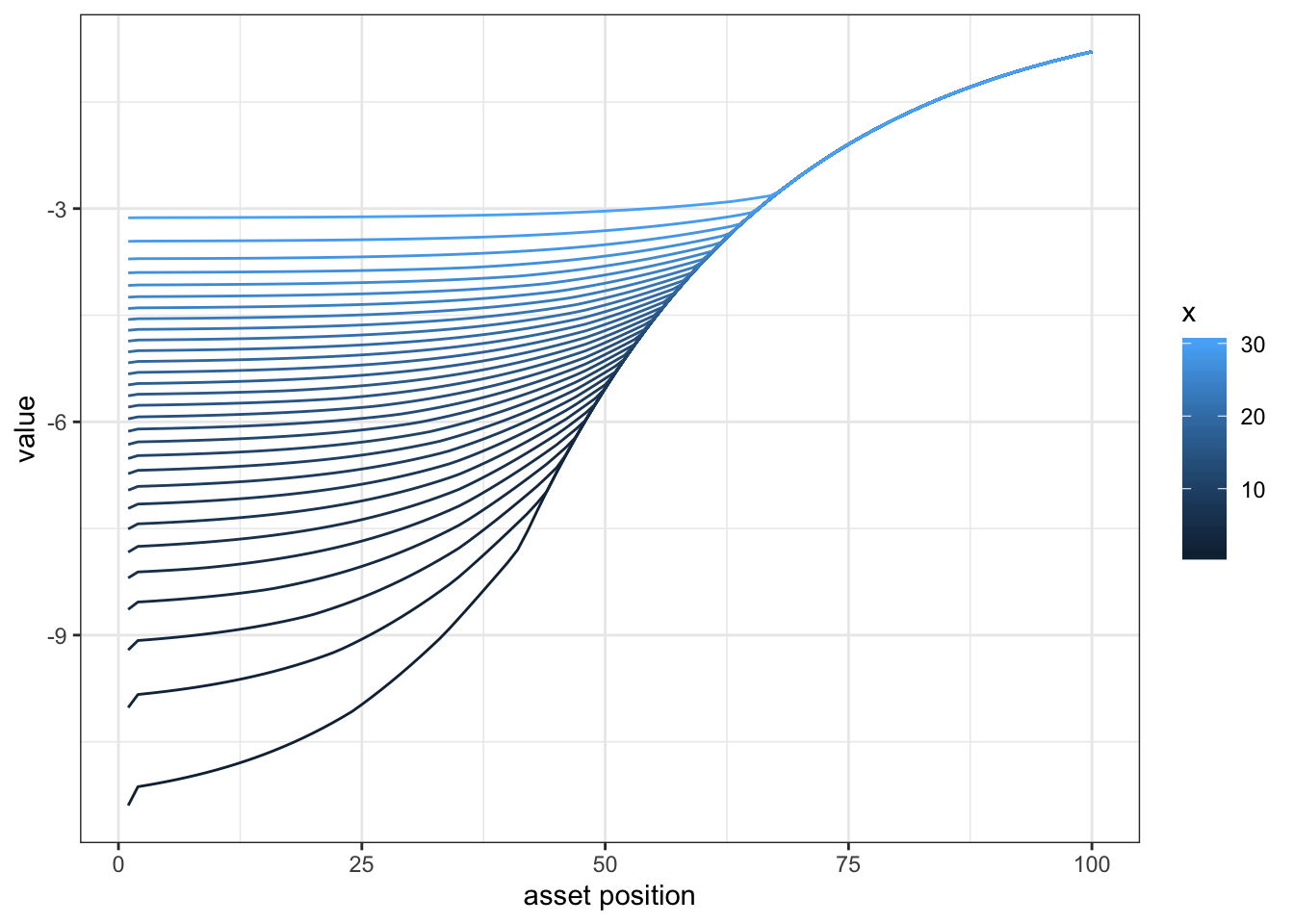

We then solve the dynamic problem recursively. In the last period, we let the agent choose a single consumption and hours value that will make asset level 0.

First step is to solve the final period problem. We assume that the agent has a access to a producitivity which is a thrid of the last period one, and then choose hours and consumption to make asset to 0.

t.final = tensorFunction(R[b,w,h] ~ ((W[w]*H[h] + r*B[b])^(1+eta))/(1+eta) - beta*((H[h])^(1+gamma))/(1+gamma) - I(H[h]>0)*fc)

VV = t.final(X/3,H,B,p$r,p$eta,p$beta,p$gamma,p$fc)

Vf = aaply(VV,c(1,2),max,na.rm=T)

# plotting the function

ggplot(melt(Vf,c("b","x")),aes(x=b,y=value,color=x,group=x))+geom_line() + theme_bw() + scale_x_continuous("asset position")

We then solve the values recursively

V[p$na,,] = t(Vf)/p$r

# prepare tensor that computes the Q value for each b,x,h,b2

t.cur = tensorFunction(R[b,x,h,b2] ~ ((W[x]*H[h] - B[b2] + (1+r)*B[b])^(1+eta))/(1+eta) - beta*((H[h])^(1+gamma))/(1+gamma) + rho*VV[x,b2] - I(H[h]>0)*fc )

B.pol = V*0

H.pol = V*0

for (age in (p$na-1):1) {

# compute expected value tomorrow

EV = Gx %*% V[age+1,,]

# compute values at each control variables

Vn = t.cur(W=X*exp(p$lambda * age/p$na) ,H,B,EV,p$r,p$eta,p$beta,p$gamma,1/(1+p$r),p$fc)

# we need to choose the asset tomorrow and hours (which then gives consumption)

V[age,,] = t(aaply(Vn,c(1,2),max,na.rm=T))

# extract policy

pol = aaply(Vn,c(1,2),function(A) which(A==max(A,na.rm=T),arr.ind = T,useNames = T))

B.pol[age,,] = t(pol[,,2])

H.pol[age,,] = t(pol[,,1])

cat(".")

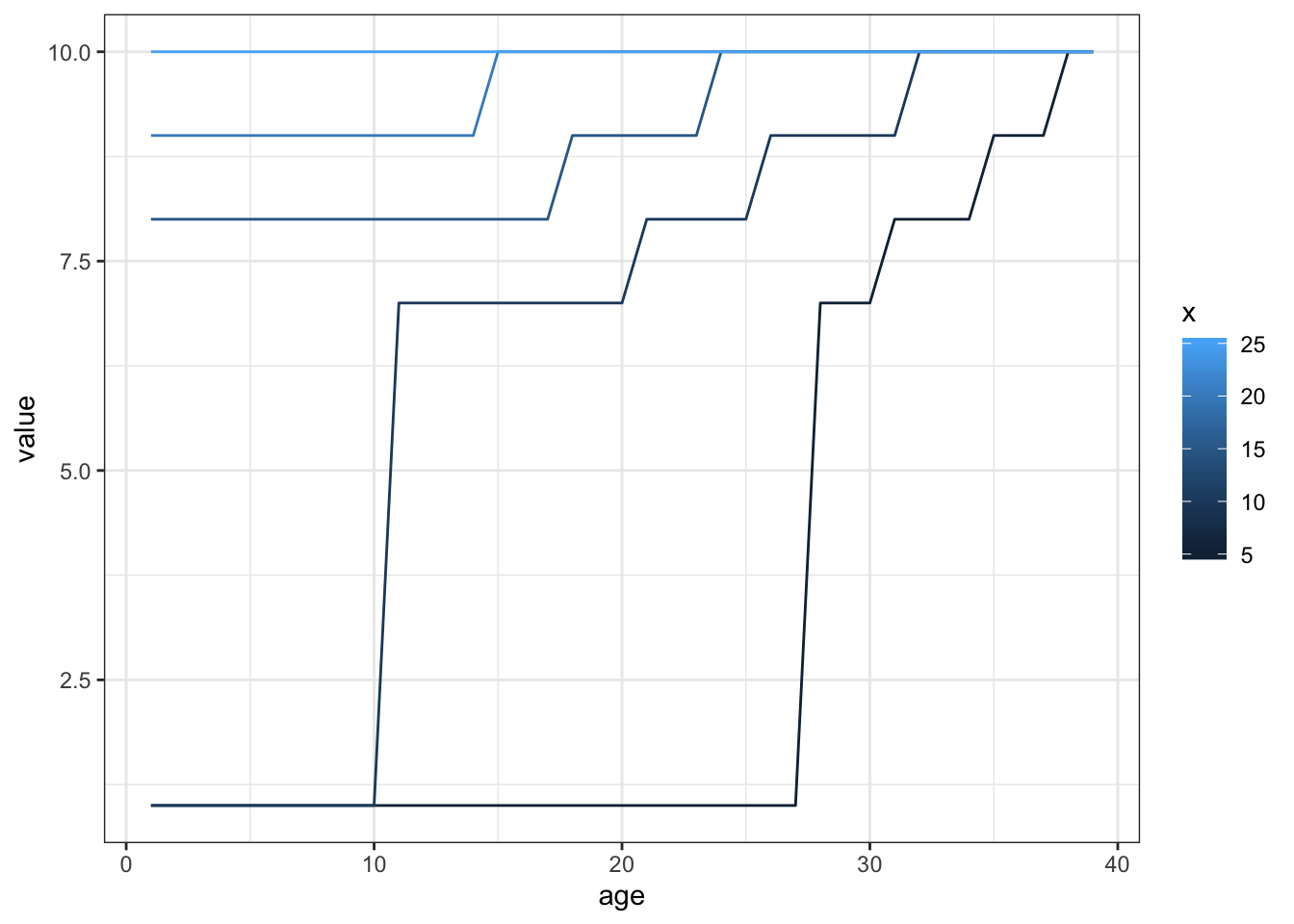

}## .......................................# let's plot hours at fix x and b over time

rr= data.table(melt(H.pol[,,25],c("age","x")))

ggplot(rr[x %in% c(5,10,15,20,25)][age<40],aes(x=age,y=value,color=x,group=x)) + geom_line()

Simulating data

Finally we simulate some data

simdata = data.frame()

D = array(0,c(p$na-1,6))

colnames(D) = c("i","x","b","h","b2","age")

for (i in 1:1000) {

x=sample.int(p$nx,1)

b=1

for (age in 1:(p$na-1)) {

x = sample.int(p$nx,1,prob=Gx[x,])

D[age,1] = i

D[age,2] = x

D[age,3] = b

D[age,4] = H.pol[age,x,b]

D[age,5] = B.pol[age,x,b]

D[age,6] = age

b = B.pol[age,x,b]

}

simdata=rbind(simdata,data.frame(D))

}

simdata = data.table(simdata)

simdata[,lw := log(X[x]),x]

simdata[,lb := log(B[b]),b]

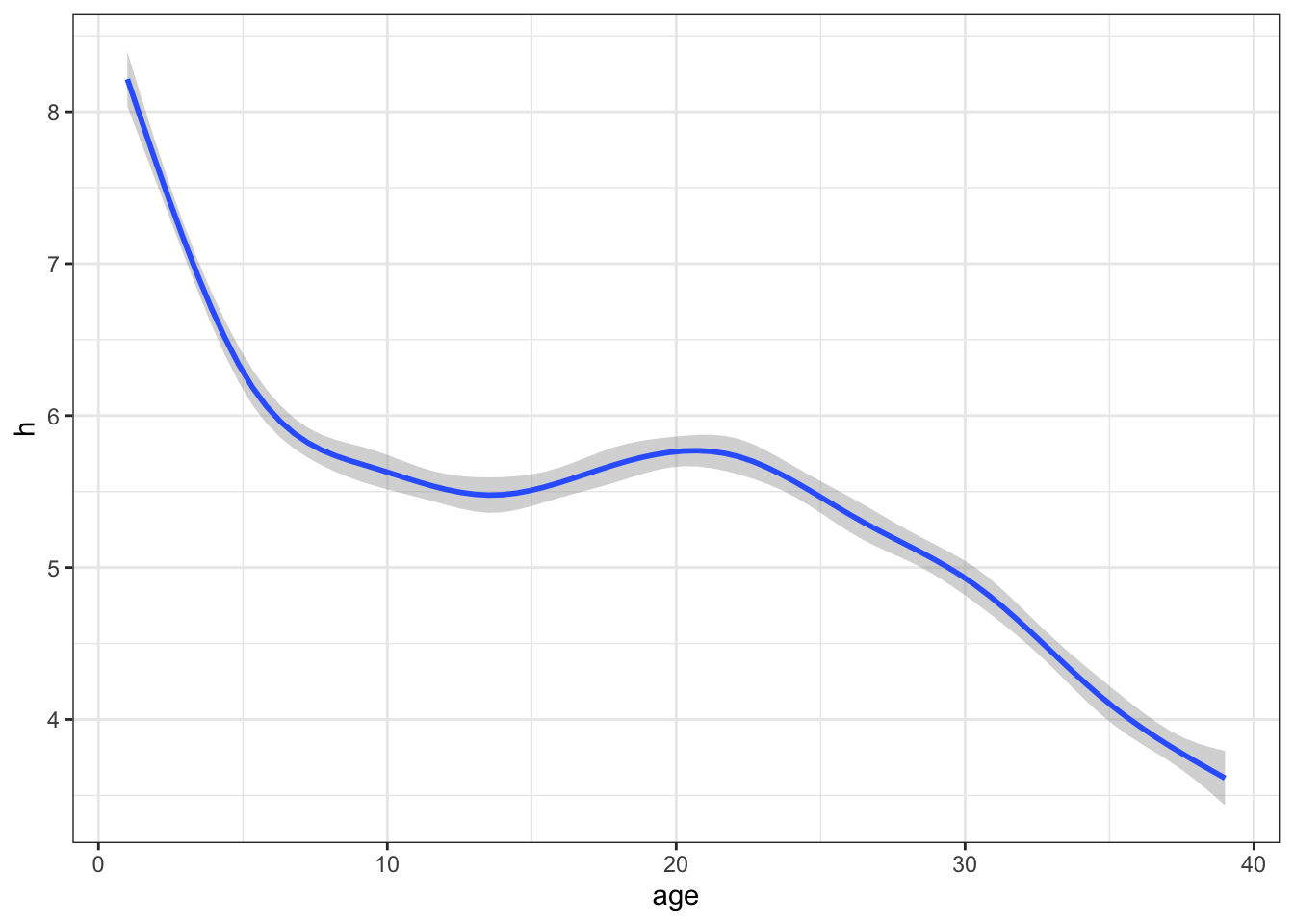

# choice of hours

ggplot(simdata,aes(x=age,y=h)) + geom_smooth() +theme_bw()## `geom_smooth()` using method = 'gam' and formula 'y ~ s(x, bs = "cs")'

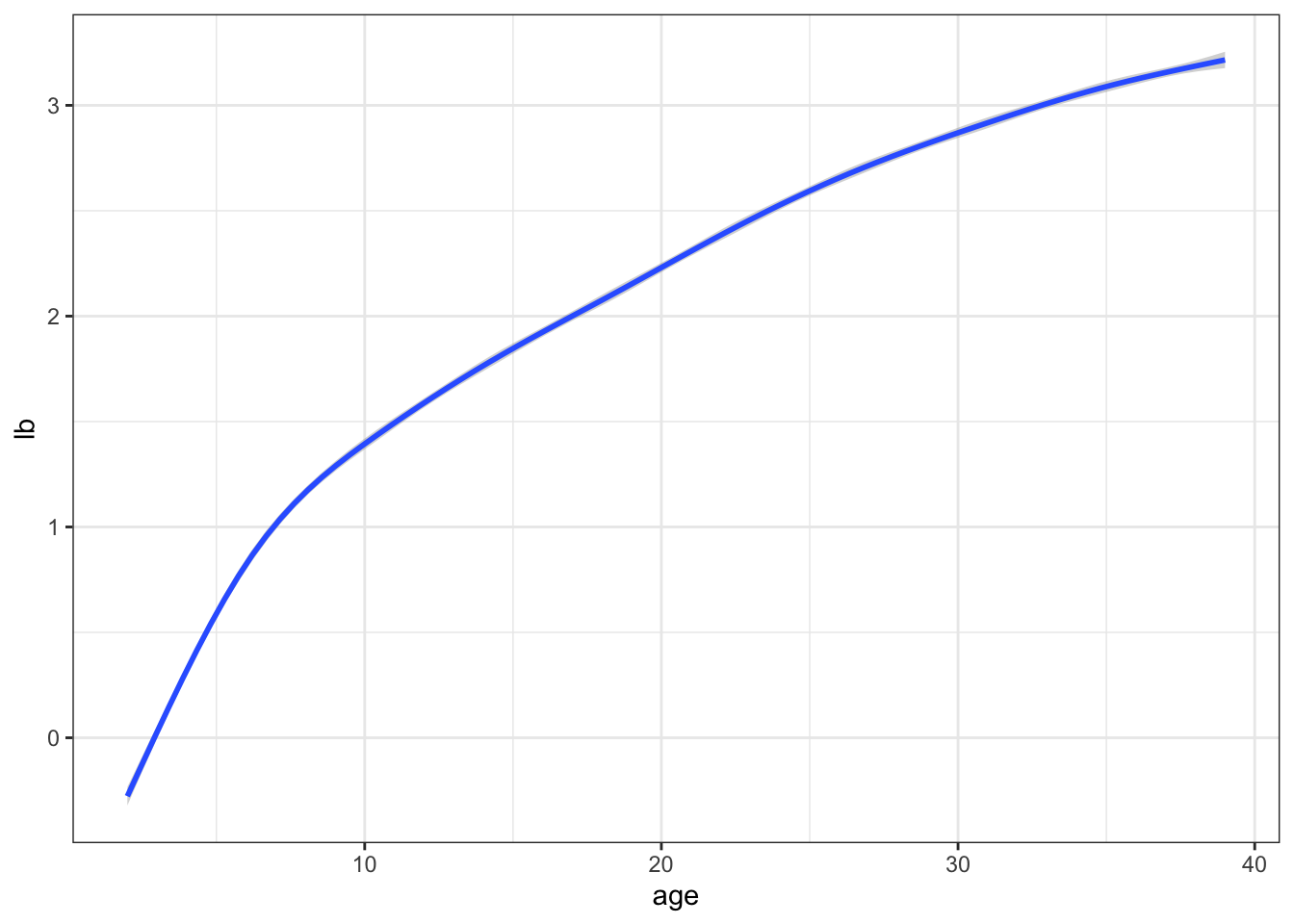

# compute asset

ggplot(simdata,aes(x=age,y=lb)) + geom_smooth()## `geom_smooth()` using method = 'gam' and formula 'y ~ s(x, bs = "cs")'## Warning: Removed 2072 rows containing non-finite values (stat_smooth).

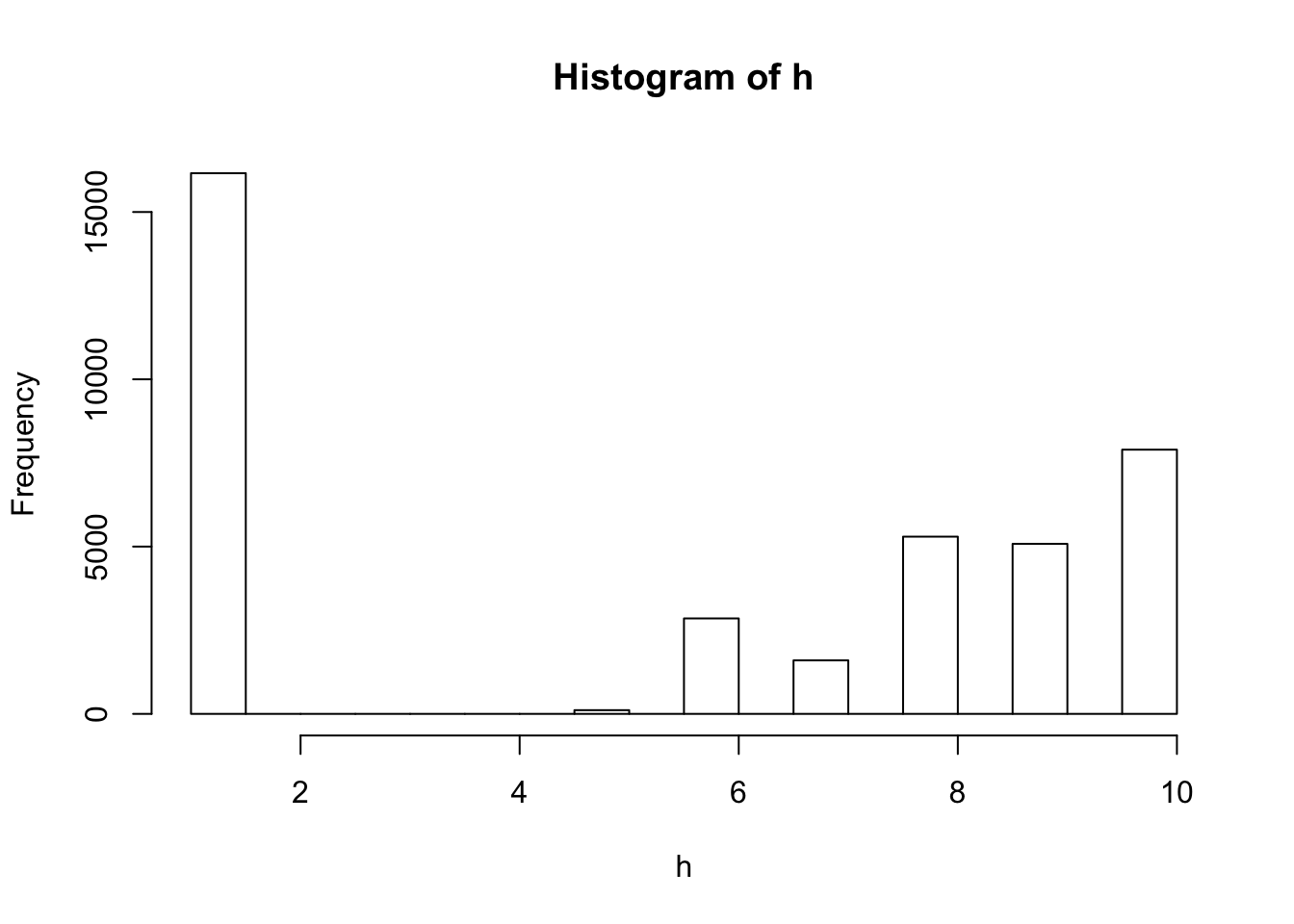

simdata[,hist(h)]

## $breaks

## [1] 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 5.0 5.5 6.0 6.5 7.0 7.5 8.0

## [16] 8.5 9.0 9.5 10.0

##

## $counts

## [1] 16161 0 0 0 0 0 0 111 0 2853 0 1599

## [13] 0 5297 0 5082 0 7897

##

## $density

## [1] 0.828769231 0.000000000 0.000000000 0.000000000 0.000000000 0.000000000

## [7] 0.000000000 0.005692308 0.000000000 0.146307692 0.000000000 0.082000000

## [13] 0.000000000 0.271641026 0.000000000 0.260615385 0.000000000 0.404974359

##

## $mids

## [1] 1.25 1.75 2.25 2.75 3.25 3.75 4.25 4.75 5.25 5.75 6.25 6.75 7.25 7.75 8.25

## [16] 8.75 9.25 9.75

##

## $xname

## [1] "h"

##

## $equidist

## [1] TRUE

##

## attr(,"class")

## [1] "histogram"